Behind the Scenes of a 502% Excess Return System (Revealing My Unfiltered Monthly Return History)

A complete breakdown of 10 years of wins and losses from the MarketFighter Strategy.

Hi Friends 👋

I hope you’re all enjoying the summer! I’m currently on vacation in Italy with my wife and our two boys. I prepared most of this post before we took off, but I didn’t want to keep you waiting until we’re back home.

This post is about returns, psychology, and transparency. Unfortunately, in finance, it’s common to only display the wins and the good parts. I strongly believe that trust is built by communicating transparently about wins as well as losses.

That’s why I’m now presenting the full return breakdown of my strategy for every single month during the past 10 years. I will compare these to the market and you will see exactly when it did well and when it did not.

New to The MarketFighter Strategy?

I write about a simple approach to beat the stock market with only 15 minutes of monthly work that anyone can copy. Check out these links:

Open track record

Actually, you don’t see this a lot in finance: A long-term open track record, revealing the performance of all trades going 10+ years back.

Many of you subscribers have told me that the transparency of my data and the open performance reporting are among the core reasons you decided to follow along.

I am very grateful for that. And I can promise you, I’m never going to hide bad results. These are as much a part of the process as the good ones.

Most of my writing so far has been focused on comparing returns by calendar year. I like this interval because it tends to give time for temporary dips and spikes to fall into place.

But annual returns don’t show the journey and the psychological struggles that may have been present along the way. That’s why I’m doing a fine-grained rundown of monthly returns in this post.

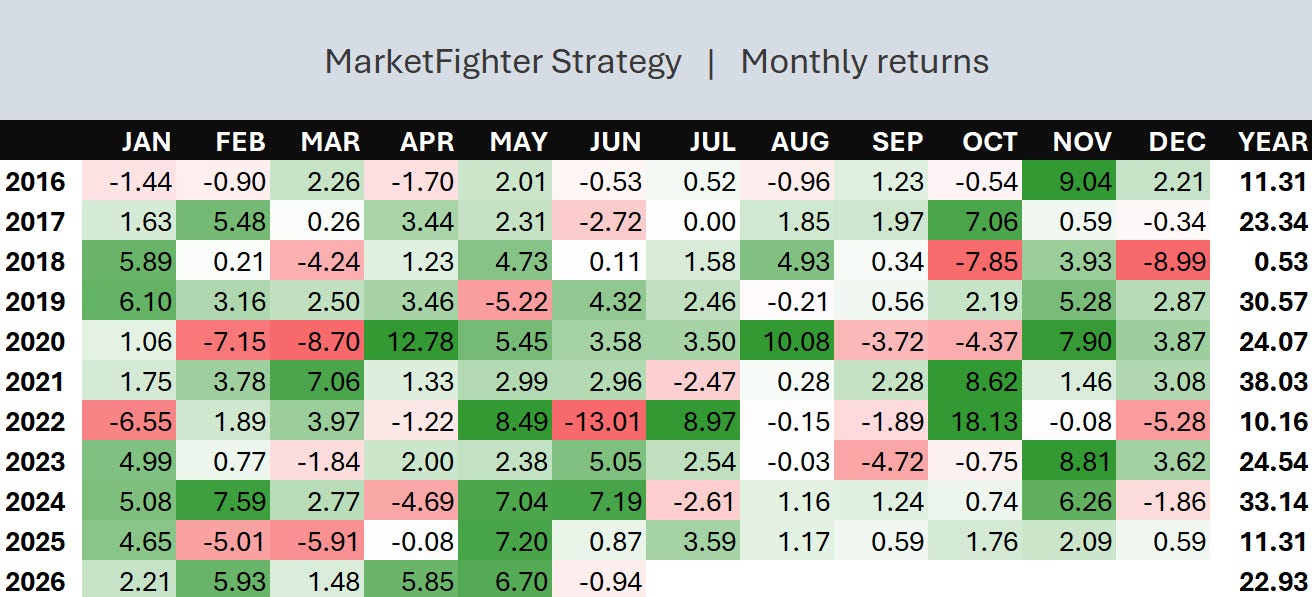

Absolute monthly returns

First, let’s go straight to the monthly returns of The MarketFighter Strategy in absolute terms (not comparing to anything else). What you see in the table below is the monthly return percentages (in EUR) since January 2016:

The column on the far right shows the returns by calendar year, which you might have seen in my other articles. The corresponding row shows the path towards it (all numbers are return percentages, not accounting for taxes and trading fees).

You will notice a lot of losing months along with the winning ones. A few examples worth mentioning:

In 2020, the strategy lost around 16% in just two months due to Covid, but managed to end the year up 24% anyway.

In June 2022, the strategy lost 13% in a single month (the worst in its full 26-year history).

In early 2025, the strategy lost 11% over the course of two months (affected by tariffs), but still ended the year up 11%.

The key lesson here is patience. No strategy wins every time. But if someone had bought this strategy and had the patience and discipline to stick to it over the past 10 years, they would have achieved a total return of 682% (not accounting for taxes and trading fees).

And just to be clear about the data: I started trading the strategy in March 2021, while all the returns up until that point are backtested based on historical index price data. You can read more about this process in this post.

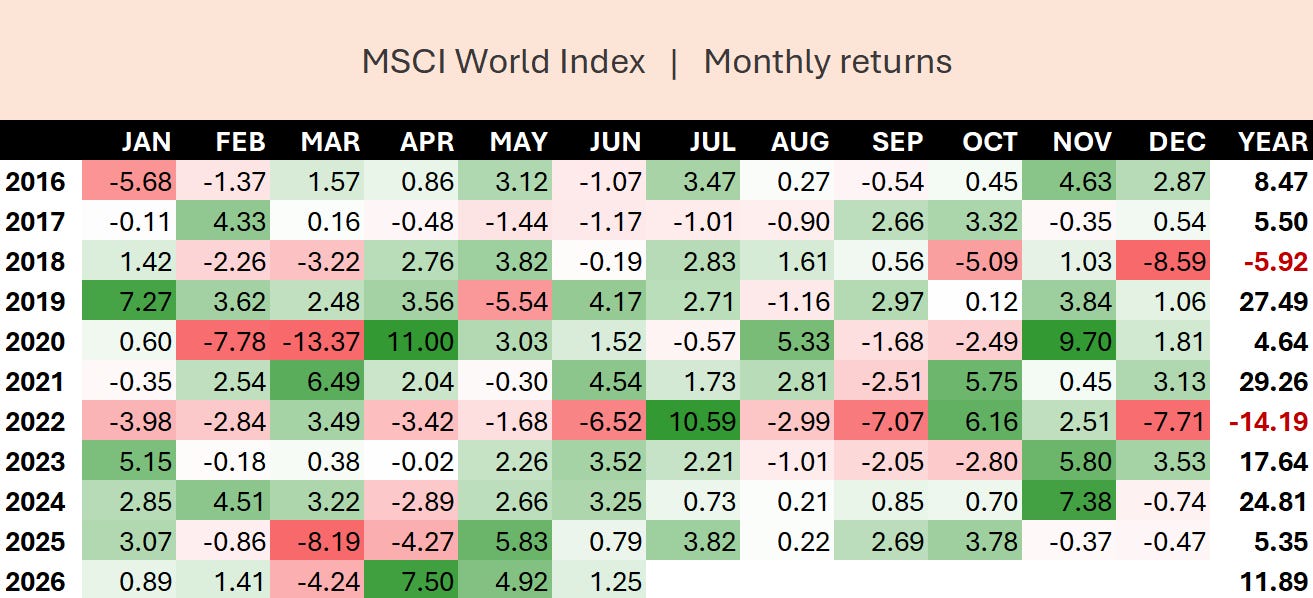

Monthly returns of the market

An honest evaluation of the performance of an investment doesn’t make sense without comparing to an alternative or a benchmark.

I’m using the MSCI World Index, because it represents the developed world of stocks which is the universe our strategy operates in.

I’m aware that many US-based investors are used to benchmarking against the S&P 500, but since it only covers US stocks, it’s not fully representative in this case. (I’m planning to write a separate post in the future focused on S&P 500 and USD.) Keep in mind that roughly 70% of MSCI World actually consists of the S&P 500.

Here’s the breakdown, exactly as before, but now for the global stock market (EUR):

The first thing that pops out is the two negative years (2018 and 2022). But looking closer, you will notice that the market experienced more negative (red) months than the strategy.

Positive months (2016-2026)

🟢 MarketFighter Strategy: 78%

🟡 MSCI World Index: 69%

But when looking at the table month by month, it doesn’t look significantly different from the returns of the strategy, does it?

The big difference is hidden in the long-term compounding, which looks easy on paper but can only be achieved by the disciplined and the patient:

10-year returns (2016-2026)

🟢 MarketFighter Strategy: 682%

🟡 MSCI World Index: 180%

Comparing these two numbers, we get a 502% excess return over the full 10 years.

By the way, for those who are curious about how the S&P 500 did over the same 10-year period, I’ll give it to you here: 313% return.

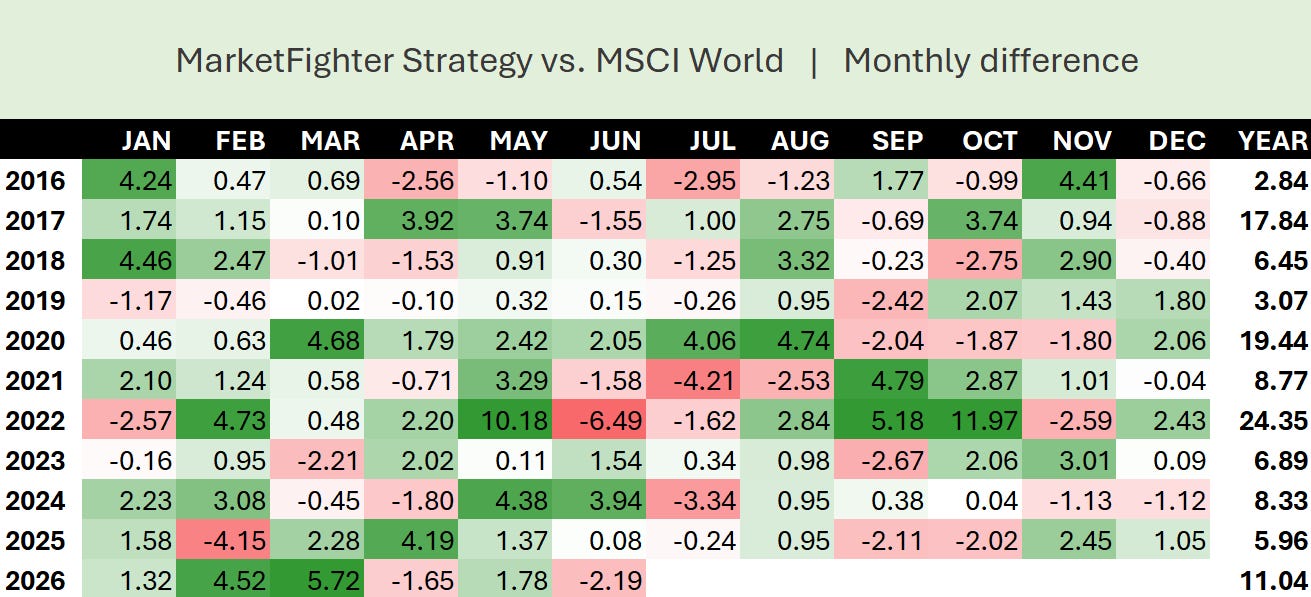

Relative monthly returns

We have now looked at the returns of the strategy as well as our benchmark in isolation, but the best way to compare them for full transparency is to look at the relative monthly returns.

Relative in this case means the returns of the strategy relative to the market or compared to the market. This is the monthly difference (aka. the alpha) achieved by the strategy over the benchmark:

Remember, the numbers here are not the returns delivered by the strategy. They’re the outperformance delivered month by month when comparing to the market.

Let’s dig in to a few noteworthy periods:

Although 2020 was a tough year for the markets due to Covid, the system outperformed in every single month until September.

A few times, the strategy has underperformed the market 3 months in a row (2019, 2020, 2021), but each time it ended up beating the market for the full year.

The worst relative month of the past 10 years was June 2022 where the Energy sector reversed after a great May, resulting in an underperformance of 6.49%.

Things become clearer when you zoom out and look at it from a bird’s-eye view. Now we see that the vast majority of squares are green, which means the strategy beats the market in most months:

Head-to-head monthly wins (2016-2026)

🟢 MarketFighter Strategy: 71%

🟡 MSCI World Index: 29%

The takeaway

Most of us suffer from recency bias. This means we value the most recent events or data over historical context. The most recent memories are the freshest, and it skews our judgement, making us believe that “this is how things will continue”.

When evaluating an investment strategy, it always pays off to look at it from a high level and keep the historical context in mind. Spikes, dips, and outliers are not uncommon in the short term.

The long term reveals the true value. Anyone can pull off a period of great returns for a year or two, but always check the long-term results when evaluating a strategy.

Whenever I feel doubt about my strategy after a bad month or two, I look at the historical data. It reminds me that underperformance and losing months are common. No strategy wins all the time.

What really matters are two things:

✅ You trust your strategy to do better than the market in the long run.

✅ You haven’t found another strategy with a higher expected return.

If you like what you read here, I hope you will consider subscribing for more investment insights and strategy. If you want full access to the monthly trading signals of the strategy, simply upgrade to join the community of MarketFighters.

Thanks for reading!

Disclaimer: The MarketFighter Strategy is for educational and informational purposes only. It is not financial advice, and the author is not a licensed investment advisor. Investing in ETFs involves significant risk, and past performance is never a guarantee of future results. You are solely responsible for your own trades and financial outcomes. Read the full Disclaimer here.